Capital Distribution:

- 1% Cash

- 97% Share in SGX

- 42% in 1 high pay Reit (13.8% DPU)

- 55% in 2 different Companies

- Annual div payout based on current PF is ~6.2%.

Since the first review on 15th May, i had made some changes to my portfolio, the main reason behind is to streamline my portfolio and focus on fewer counter that i'm confident with.

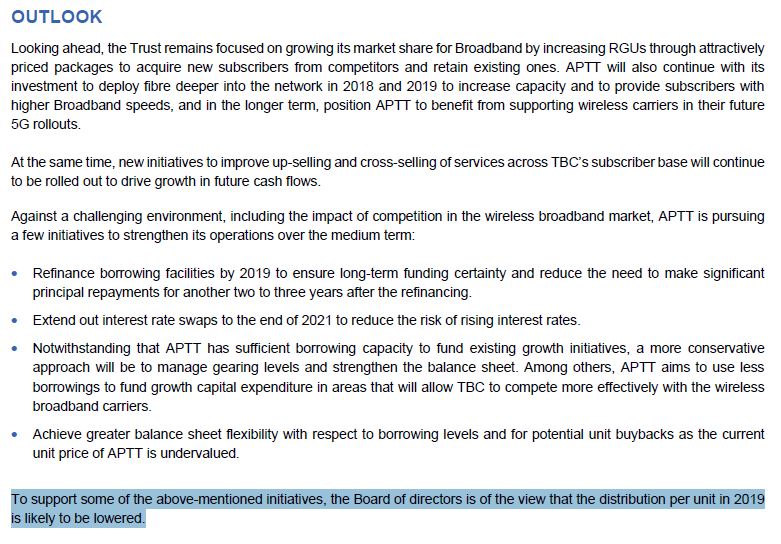

1. Asian Pay Tv:

I had made a transaction to average down this reit at 0.46c, of cause, that is before it went down to ~0.41c and now come back at weaker momentum. My current avg price is at 0.54c with paper loss of ~19%. To be honest, the situation is ugly, i have to admit that, i'm only looking at the high DPU of this counter (~12.2% at my avg price), other than that, the situations of the company are not that attractive with the high gearing and challenging business environment. 2 key challenges for the company are: the popularity of internet Tv in the future over current cable Tv, and the tax rule changes at Taiwan (increase from 17% to 20% for related business), which had significantly impacted the profit of the company.

Well, the situation is still in mix, as the company have an advantage of 100% owning the hybrid fibre coaxial cable network in their franchise areas of Taiwan (Taoyuan, Hsinchu, Miaoli, TaiZhong), owning this facility have add advantage to the company in the sense of:

- Building the Fibre cable is a resilient business with high barriers of entry due to high network roll out requirements.

- Large customer base makes TBC attractive to local content providers; unique commercial arrangement with content providers.

- Long standing relationship with subscribers; deep understanding of Taiwanese viewers’preference.

How i look at the situation is: although there will be a hard fight between internet Tv and cable Tv, the high quality internet will need to rely on the broadband, which is backed-up by the hybrid fibre coaxial cable network. So, with regards how bad the fight is, Asian Pay Tv should also get some return from their cable network. A good news is that the broadband business is the only business that seeing growth in the latest quarter, which at least re-leaf my short term worried on this counter.

2. Avi-tech.

I disposed all my Avi with several reasons:

- Wth the same DPU at ~5%, Singtel seems to be having more advantage in terms of the share price and the business model.

- I entered Avi without much advantage of the share price, and the latest Quarter report shows decline in the profit, indicates by the weaker demand of electronic testing. So cutting out this counter at 9% loss and work it out as per the plan.

3. Singtel

No doubt, Singtel share price declined after they announce the latest quarter report due to the profit are not meeting the market expectation. With the original plan to avrg down at 3.2-3.3 and cut loss at 3.0, i had top up some units at 3.29 (after seeing recovery from 3.24), unfortunately, the share price went back down again recently to 3.23. My average price is now at 3.4 (~5% paper loss), but i have no worried about this counter at all: a blue-chip with share price @ 52 wk low + 5% DPU + good management + Temasek holding... hahaha... This will be my long term game.

4. Hanwell

This is really a boring counter, but i had decided to top up more at 0.23c, it is at net net stock at this price. The company have 2 key businesses: A good growth sector from their paper packaging business, and a stable + solid business sector from their FMCG (rice, toufu, snack and bla bla bla....). There is a lot of potential for the share price, and relatively lower risk due to the good FA.

That is all for the changes in my portfolio, now i have a high DPU Reit (relatively high risk

:(

:(), a superb bluechip stock and a low risk net net stock, i'm very comfortable with the arrangement. I guess the missing type of counter in my portfolio will be a high growth mid cap stock. lets reserving bullet while continue searching for my last piece of puzzle!