+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

投資致富 2012-12-10 11:25

芙蓉讀者問:

輝德控股(FITTERS,9318,主板貿服組)前景如何?我早前以每張5仙,買進20萬張輝德控股WA(FITTERS-WA,9318WA,憑單),若全面轉換這批憑單,虧損幾率會有多大?因為我擔心當每個投資者都進行轉換,賣壓會導致轉換成本上升,最終母股會跌破58仙嗎?

答:

輝德截至9月30日首9個月淨利增長18.13%至1千754萬4千令吉,受惠於防火配備及建築原料銷售上漲。雖然該公司一直以來都取得盈利成長,不過卻沒有受到市場太大的關注。

該公司早前與貿易風種植(TWSPLNT,6327,主板種植組)聯營投資綠色提煉廠解決方案活動,將提煉廠排出的污水和棕果渣用於發電和生產纖維。這符合其商業經營模式,除了透過纖維貿易營造經常性收入,也藉此增加收入基礎,相信上述投資項目每年可捎來150萬令吉淨利。

分析員認為輝德攫獲的綠色提煉廠解決方案合約,只能從2013財政年開始顯現盈利效益,並看好該公司未來將宣佈更多類似投資項目,以吸引機構投資者的目光。

綠色提煉廠業務料佔2013財年7%盈利貢獻,但2014年可激增至29%,至2015年更達41%。該公司整體表現不錯,分析員給予其1令吉零5仙至1令吉15仙合理價,不過若缺乏催化劑,股價短期或難有大突破。 (good to catch now :P)

另外,談到憑單轉換問題,輝德控股WA已從11月8日起暫停交易,並在11月28日除牌。以53仙轉換價及你買進的每張憑單5仙計,總成本只有58仙,顯著低於母股約64.5仙。兩者的價差為6.5仙,若乘上手中的20萬張憑單,則可在轉換期限內賺取1萬3千令吉,惟前提是母股仍企於64.5仙水平,而上週五止,每股只處61仙水平,未來盈虧仍胥視母股前景。(星洲日報/投資致富‧投資問診室)

+++++++++++++++++++++++++++++++++++++++++++++++

So, the mother seem to be more attractive to me compare to the WA, even though it is not applicable now, i more interested in the comment of the future earning.

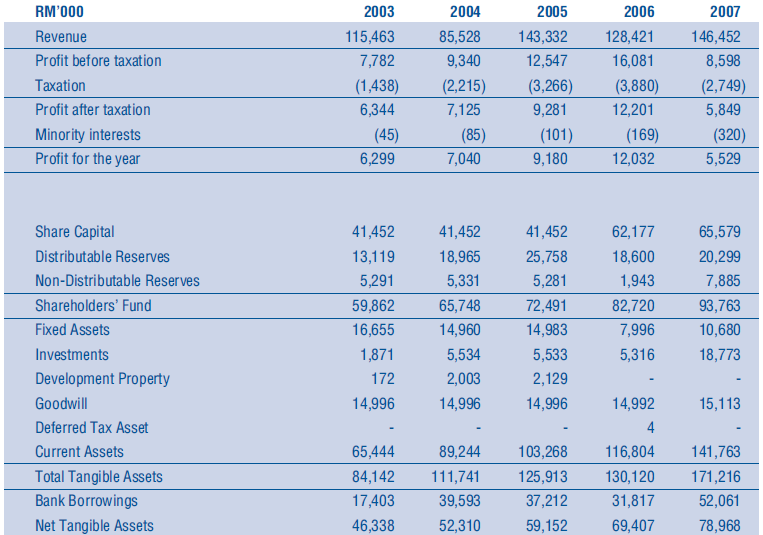

Digging more into the annual report to check out the performance again, as in my previous post, the performance of this stock is consider fare, however, I'm interested to look into more on the company performance during 2007/2008 and 2009 to check out how did she perform during financial crisis, well, this is what i found:

Summary:

1. Company is making profit for pass 10 years, non of the year is making loss.

2. EPS & profit is fluctuating, but still performing at average during 2008/2009 period.

3. Revenue increase in recent 5 years, latest rolling 4 quarters shows slight drop in revenue (404,607) as compare to 2011 but profit is higher then 2011 with rolling 4Q ended at 24,668 (EPS ~11sen)

4. historical gearing looks healthy and well below 0pt5. just a bit concern on the operating cash flow over total asset, it was at -ve on year 2011.

5. ROE not really stable but still +ve.

From business point of view, it is the leader in providing integrated fire protection and prevention solutions as a “one-stop” fire protection specialist. In mid of 2011, the company start to expend into the renewable energy & green palm oil mill, property development and construction engineering which is still a good move from my point of view (anyhow you can only make consistent money with concurring the fire protection market in Malaysia, to growth the company, i think this is a good move).

looking at the top 30 share holder list, they are holding up to ~70% of the share at 2011, the liquidity of share in the market is quite low if it is still in the same status today. Also that the company still carry out quite heavy of share buy back in this year and recently, not sure this is good or bad but at lease this shows that the share holder are still confident on the business (given it to maintain the share price or to accumulate the share)

Good thing is it is not a hot stock and i don't think the market is focusing on this counter, current price at 0.61sen with PE at ~8.7, not super cheap but it has been traded at 2 years lowest price now. current CPO price is pretty low, and by the time the CPO price recover, i would expect the company will be making profit from the green energy division.

FITTERS was introduced by SAM, together with the same time frame, he had also buy in some other stock, however, I only intrested in FITTERS mainly due to what was discussed above. I'm currently holding FITTERS with less then 20pst of my capitial, i'm going to try to swap some of my warrant to FITTERS and make it to about 30pst of my capital, this will be my 1st step to change my invesment from heavy warrant to heavy mother :P

- Just a 2 sense from me :)

No comments:

Post a Comment