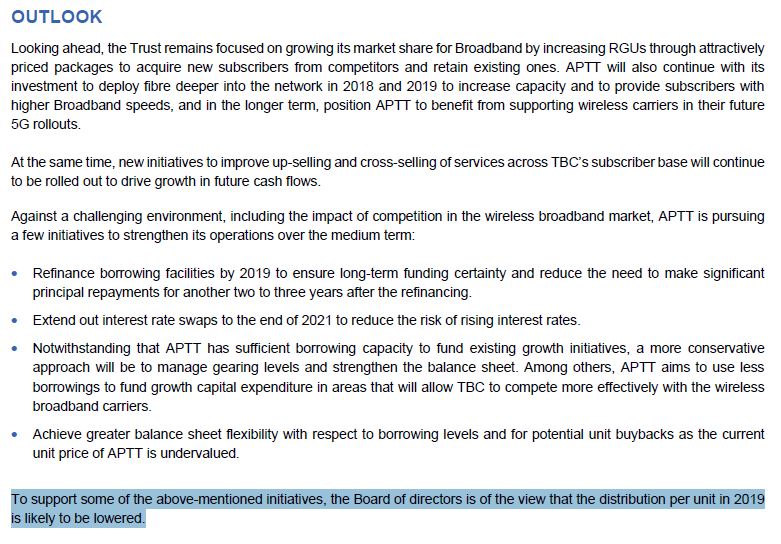

The main activity for this week is to dispo my Asian Pay Tv. It is sad but is a must do with the reason that i shared in my previous post. After i dispo the Asian Pay Tv, i quickly SWAP to some other stock. Fajar and Malton are the 2 stocks that quickly take up my capital from the disposition of Asian Pay Tv. Why Fajar and Malton? first of all, this 2 counters were mentioned in the "Rainmakers", well, thanks to the page and i stretch a bit to check out the feasibility to invest in this 2 counters. Together, i put in a fundamental comparison with Ekovest, Destini and WCT as well. Again, the goal is to look for Malaysia MID CAP developers who have good fundamental, good earning capability and reasonable dividend pay out.

Above data captured from 7th Aug (all except Ekovest) to 13 Aug (Ekovest) through investing.com. can see that Fajar and Malton are the top 2. Based on market CAP, WCT is not really the same batch with the rest and i put it in just as a refferance since it is one of my closely monitored counter.

Fajar have a mix business with additional income from Timber, so to be honest, by putting Fajar in the list to compare is really not an apple 2 apple comparison but rather orange and Mandarin orange comparison. As for Malton, it comes with the honer from Pavilion and some good project on hand is definitely some positive point for it. another key reason for selecting this 2 is, they both have the top 2 highest dividend payout based on current price. In view of their trend, both had kind of recover from bottom with >10% recovery liao, enter at this point will be more comfortable for me since the trend shows recovery and not batting on the re bounce.

Fajar

Malton

For the strategy, the capital from Asia Pay Tv will be divided into 2 and invested in Fajar and Malton @ the price of RM 0.495 and RM 0.655 respectively. Any cut loss? based on the trend and EMA, Fajar should cut at 0.485 while Malton should cut at 0.61, anyway, I'm not so certain about the cut loss price at this moment since the Fundamental for this 2 counters are reasonable to hold for mid to long term with current enter price. Both counter will have their quarter result published in Aug'18, so lets see how it goes.

Below is my updated portfolio:

Key Notes:

Swap from Asia Pay Tv to Fajar and Malton, loss of ~26$ from Asian Pay Tv :(

Singtel reported their latest Quarter result on 8th Aug with drop in revenue, share price impacted immediately since 10th Aug.

Hanwell reported their latest Quarter result on 13th Aug, which is higher than Q2'17, today is the first day the share price reflected the good news.