APPTV just announced their latest quarter report, such a disapointed result. Infact, it is not totally unexpected, this is what capture from the latest Q-report end 30 Jun 2018:

In constant Taiwan dollars (“NT$”), revenue down 4.1% for the quarter and 4.9% for the half-year as foreign exchange contributed 2.5% negative variance for the quarter and 1.8% for the half-year

- Basic Cable TV: Down 4.6% for the quarter and 5.6% for the half-year in constant NT$ terms mainly due to lower subscription revenue, driven by marginally lower number of subscribers and ARPU compared to the pcp, and lower revenue generated from channel leasing partially offset by higher airtime advertising sales.

- Premium Digital Cable TV: Down 10.4% for the quarter and 9.2% for the half-year in constant NT$ terms. Generated predominantly from TBC’s average Premium digital cable TV RGUs each contributing an ARPU of NT$133 per month during the quarter for Premium digital cable TV packages, bundled DVR or DVR-only services.

- Broadband: Up marginally for the quarter and remained broadly unchanged for the half-year in constant NT$ terms. Generated predominantly from TBC’s average Broadband RGUs each contributing an ARPU of NT$439 per month during the quarter for high-speed Broadband services.

Below table tell a better story:

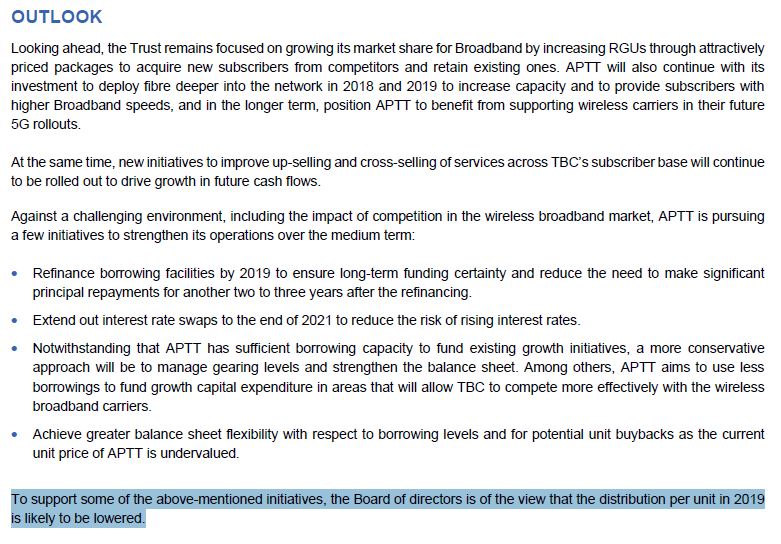

A sad part from the report is below highlighted statment were spotted in the Outlook statement:

==> To support some of the above-mentioned initiatives, the Board of directors is of the view that the distribution per unit in 2019 is likely to be lowered.

My intepretations:

1. The situation is bad, management have no confident to recover the weak performance.

2. DPU lower always not a good thing for me.

A side thought: Do youconfident that APTv can recover the situations by cutting the DPU and with above plan? It all went back to the business that APTv is doing. With that says, i had decided to cut loss at this point, sold off all i have @ 0.40 and take the loss of ~26%. A simple reason, APTv have no longer meet my needs as the future DPU is not secure, so just cut and move on.

I had swap to some Malaysia construction counter. update in next blogging.