我回来啦!!沉静了两年,我人生中发生了很多事,买了房,结了婚,在加上频密的出国公干,我竟然荒废了Blogspot, 哈哈。。Update一下status, 两年来,起起伏伏,在2012年年尾,我好像发现了一些心得。。。我还是不适合频密地交易。。看看以下我的Record:

还是写英文比较方便,虽然是Broken English...hahaha

Review the performance for last 2 years (July 2010 - Dec 2012), although i still have a net gain of ~8%, but this is just like putting my money in the FD!! WTF!! and what i observes from this history is the gain can only comes with long holding time + low/ fair enter price, look at FAVCO, BOC, and Puncak!! average PE at that time is ~4-5! solid company with consistance gain!

How about those i sell with loss? common is i'm not confident to these company and i sold them out each time i hear any bad news, to check back again whether what is the performance of these stock, lets look at it one by one.

Sealink:

EPS continue drop from 2008 - 2011, with roling 4 Quater result, looks like 2012 EPS continue to reduce to 2.58, this mean profit continuously drop for 6 years, while overall market recover in 2010 but the earning of sealink do not follow, i cut loss at RM0.60 with the net loss of 17% :( what a bad buy in move... should see the earning shrink across 2008 to the time i buy in.

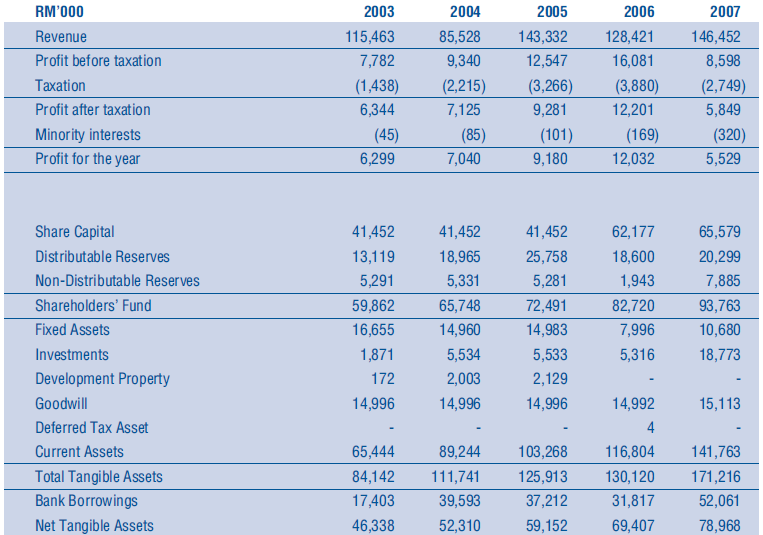

FAVCO:

EPS continue growth from 2008 even up to this year, PE when i bot should be ~5-6, now is ~7 :) shere price stod at 1.65 now, too bad i do not have holding power, else gain is ~85%.

SCOMILA:

This burger, performance is really not stable, some more got loss on 2010 & 2011, 2012 roling 4Q still net loss with EPS at -12. although latest 3 quarter it start to recover, but overall, the company is not consistant. short term play is still able to make profit, the LA is now at ~35sen and 1X higher then my buying price, but appearantly i'm not the kind of person that able to pick the gain from this stock, haha..

BJCORP:

This is a big company, but the CEO reputation is not good, the profit also marginal and seeing loss at 2009. lets see why i buy this stock (luckly i do record :P)

Catching chance?! predict future?? haha.. Now this is not a good reason to buy in:

1. Gain still not stable along the time, EPS droping, so it is not a good way to predict the future of the company with not so excellent history data.

2. PE high when the time i buy, it is at ~11. current price is ~50cts, PE ~8

I dispo all at RM1.04, how lucky am i ?!!

HUNZPTY-WB:

This stock looks good in earning,continue increase in profit since 2008, too bad that i'm buying the WB previously, current PE is ~2, Maybe this can be one of the counter that worth to invest. KIV KIV :)

BOC:

This is the stock that teach me a lot, bot in by following SAM and doing so study after that, 4th largest Bank in China, one of the China bank that have more investment in the global market. Price deep to <2 .5=".5" 2008="2008" 2010="2010" 3.4hkd="3.4hkd" and="and" at="at" back="back" bad="bad" boc="boc" brought="brought" buy="buy" crisist.="crisist." current="current" dip="dip" do="do" drop="drop" due="due" euro="euro" even="even" finance="finance" future="future" gainning="gainning" haha..="haha.." have="have" holding="holding" i="i" in="in" increasing="increasing" is="is" it="it" mainly="mainly" market="market" nbsp="nbsp" near="near" not="not" p="p" pe="pe" power="power" price="price" some="some" that="that" the="the" time="time" to="to" too="too" when="when" will="will" with="with" yearly="yearly">

TAMBUN and KSL:

Tambun is a newbee to the main board, KSL is a stable company, both of them is a fair counter, KSL profit up up down down, but still no loss, not bad, Tambun have less history data, need KIV, tambun is now with PE ~9, higher then my buying price.

Overall, with the bad trading history in this 2 years, the conclusion i have is that

1. I'm not suitable to use the "low buy high sold" method, i do not have a full time analysis on the stock and full time monitoring the stock price, thus not suitable to catch the best price.

2. Warrent is not suitable for me, if i have no time to monitor the share price, mean i might need to hold the stock for some time, holding the monther vs warrent, looks like mother is more confortable, of cause, blue chip warrent can be consider.

Current holding stock are YTLPOWR-WB, PJDEV-WC, HAPSENG-WA and FITTER

YTLPOWR, is a cash rick company, with PE ~9, cattching the WB seems more reasonable for me.

PJDEV-WC, this is highest paper loss for my combi as of now. this is a fair counter, my WC might be buying at higher price, for now i can only hold.

HAPSENG-WA, this is also a fair company, marginal paper loss, current PE at ~9, hold for a while.

FITTER, PE at 8.5, also a fair company. hold and see.

Looking at current holding, 75% is warrent?! hmm... my target for 2013 is to swap from warrent to mother stock... :)

Coming up stock selection will be focus at Mother stock, low PE, continueous earning.